0%

0%

On January 17, 2012, Puerto Rico enacted Act 22, known as the “Individual Investors Act.” This Act was designed to help accelerate the economic recovery of Puerto Rico by attracting high net worth individuals, empty nesters, retirees, and investors to relocate to Puerto Rico.

In short, Act 22 provided 0% capital gains tax for gains you realize after moving to Puerto Rico, assuming you also satisfy calendar year bona fide residency requirements (as determined by the IRS). This is all possible because the Federal Government does not tax Puerto Rico residents, instead leaving that responsibility to the Puerto Rican government.

As of January 1, 2020, Act 22 has been replaced by Act 60, which brings with it some changes to the requirements. In this guide, we outline the changes Act 60 has made to Act 22.

There is a separate act for businesses called Act 20, which Act 60 has also replaced (see our guide).

What are the tax benefits for Act 60 Puerto Rico?

Eligible new Puerto Rico residents receive the following benefits for income accrued after the individual begins to become a bona fide resident of Puerto Rico before January 1, 2036:

- 100% tax exemption from Puerto Rico income taxes on all dividends

- 100% tax exemption from Puerto Rico income taxes on all interest

- 100% tax exemption from Puerto Rico income taxes on all short-term and long-term capital gains

- 100% tax exemption from Puerto Rico income taxes on all cryptocurrencies and other crypto assets

A few points of clarification:

- Understanding the ins and outs of bona fide residency and the key dates associated with it are critical to your relocation and tax strategy. In the example of a stock, which is taxed as personal property and thus a capital gain, the date that establishes your tax basis is the date in which you commence becoming a bona fide resident; this is also known as your move date, or the date in which you cease to have a tax home in the United States. For Act 60 to kick in, you must successfully obtain your tax decree and satisfy the bona fide residency requirements for that calendar year (i.e. actually become a bona fide resident). If you do not accomplish these steps in full, all income will be taxed in the United States (more on this in the next section).

- Dividends and interest (benefits 1 and 2 above) are not considered capital gains, but rather “investment income,” because the return is not reliant on the initial capital expenditure. For investment income, the IRS considers the source of income to be where the payer, or company, is located. Therefore, unless the payer is based in Puerto Rico, you will owe U.S. taxes on investment income even after moving to Puerto Rico. See our sources of income table at the bottom of this article for more information.

You need to actually move to Puerto Rico

As part of Act 60, you need to become a bona fide resident of Puerto Rico. A bona fide resident of Puerto Rico is a person who can meet all three of the following IRS tests:

- Presence test: The individual is present for at least 183 days during the taxable year in Puerto Rico (there are other ways to satisfy this requirement). This is known as the “where are you” test.

- Tax home test: The individual does not have a tax home outside of Puerto Rico during the taxable year. This is known as “the office test.”

- Closer connection test: The individual does not have a closer connection to the United States or a foreign country than to Puerto Rico. This is known as the “in your heart test.”

We’ve devoted a separate article to explaining these tests in extreme detail – consider it required reading.

One major change in Act 60 is the additional requirement to purchase property in Puerto Rico. The grantee must purchase real estate property in Puerto Rico within two years of obtaining the decree, and the property must remain the grantee’s primary residence throughout the validity of the decree.

When should you actually move to Puerto Rico?

There has long been confusion around which date you should use to establish your tax basis on a security when coming to Puerto Rico, which in turn determines your income tax obligation. Is it January 1 of the year you move? Or your move date? Or your Act 60 application or acceptance date? For capital gains and Act 60, the answer is based on the type of income and your residency status, which is mostly determined by the IRS and not Act 60. The Act 60 component is what then exempts you from Puerto Rico income tax (e.g. Puerto Rico capital gains).

Here’s an example of a stock, which is taxed as personal property based on the owner’s tax home:

- Apply for Act 60 anytime during calendar year.

- Move to Puerto Rico and take steps to establish residency.

- Meet the Puerto Rico bona fide residency requirements during calendar year, which means you are a bona fide resident for that entire year. In general, this means you would need to move before July 1 to achieve 183+ days.

- Prove residency when you accept your Act 60 decree, thus making it effective.

For personal property like a stock, your “move date to Puerto Rico” determines the date of sourcing because your tax liability is based on the residence of the taxpayer.

Now that you have your tax basis date established, you need to determine how to allocate the unrealized gain to each jurisdiction. We say unrealized because if you’ve already realized or closed the position prior to moving, this gain is not relevant for Puerto Rico.

What if you have previously lived in Puerto Rico?

When Act 22 was initially enacted, grantees were required to have not lived in Puerto Rico for at least 15 years prior to the enactment of the law. This was amended to six years in 2017. Now, with Act 60, the period has been extended to 10 years before the Act’s effective date. This means that to be eligible, the individual must have not lived in Puerto Rico since January 1, 2010.

What about your gains before moving to Puerto Rico?

Capital gains accrued before the individual established residency in Puerto Rico (“Non-PR Built-in Gains”) are subject to preferential Puerto Rican income tax rates:

-

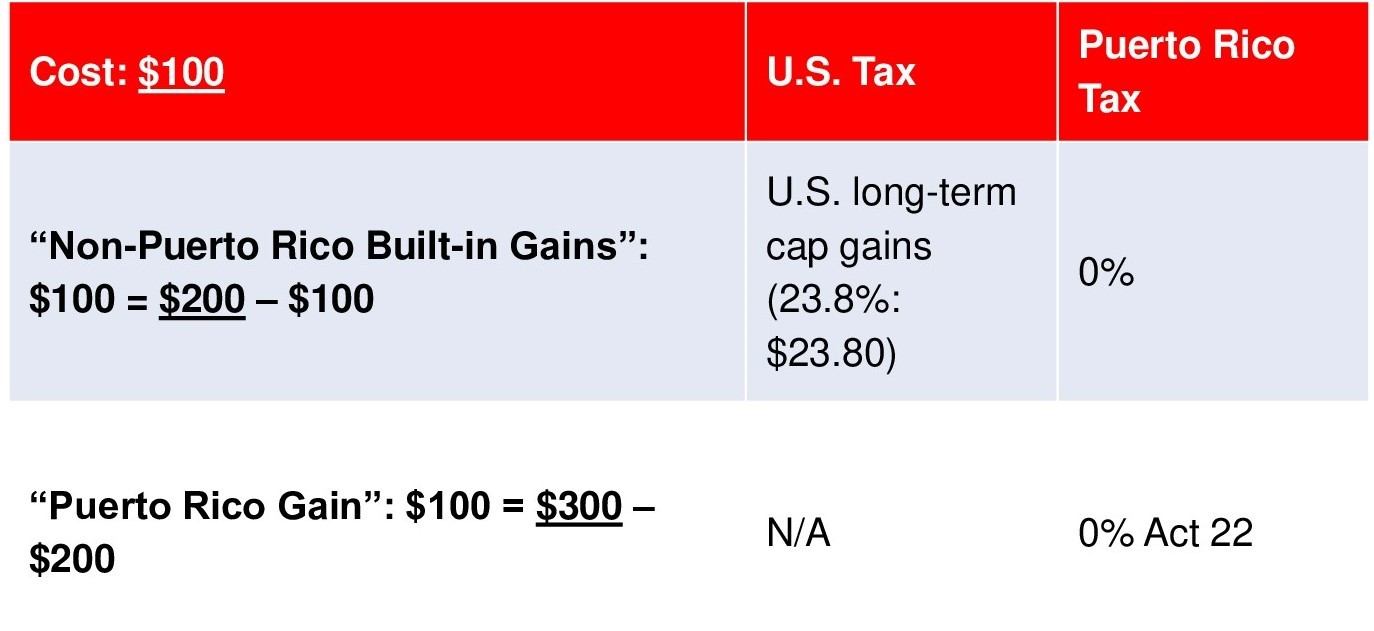

- Within 10 years – if gain is recognized within 10 years of establishing residency in Puerto Rico, it will be taxed only at the U.S. federal income tax rate for capital gains.

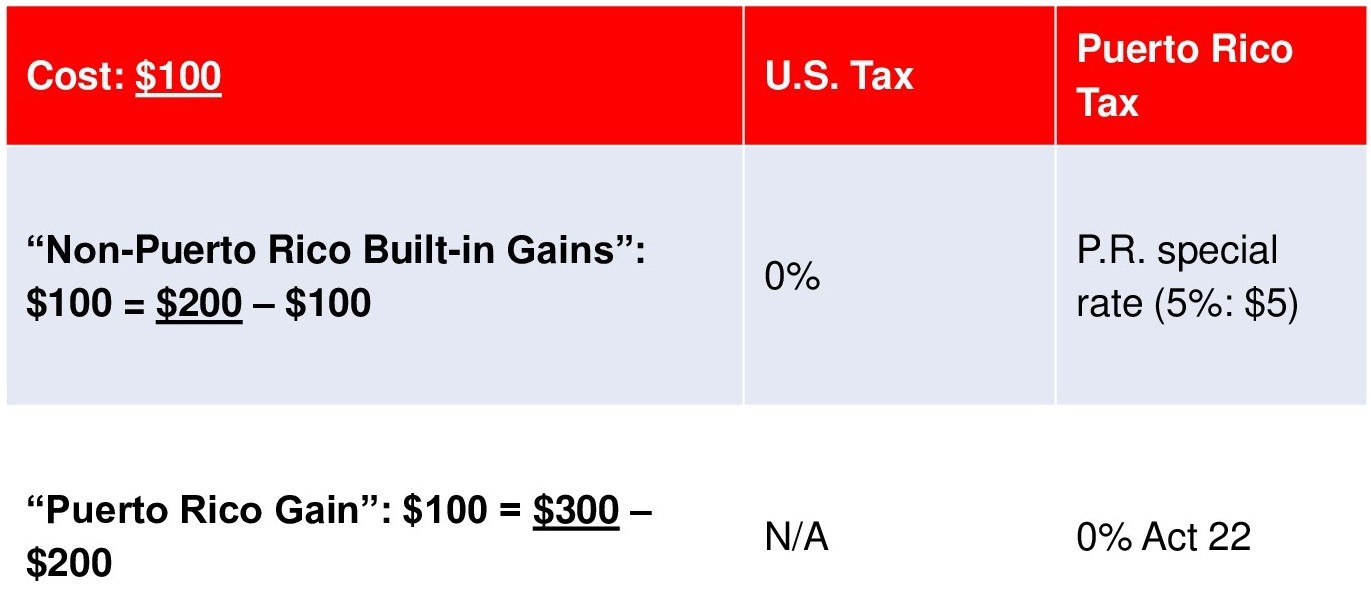

- After 10 years – if gain is recognized after 10 years of establishing residency in Puerto Rico but before January 1, 2036, it will be taxed at a flat PR tax of 5%, and the U.S. federal government will not pursue a capital gains tax.

Example 1 – Within 10 years

- A stock is acquired by a U.S. resident for $100 in 2013

- The stock is worth $200 in 2020, just before the U.S. resident moves to Puerto Rico

- The stock is sold by the now Puerto Rican resident in 2026 for $300

Example 2 – After 10 years

- Using the same scenario in Example 1

- The stock is instead sold by the now Puerto Rican resident in 2031 for $300

There are two types of securities you may need to establish a tax basis for:

- Publicly traded security (marketable) – to determine the amount of “non-PR built-in gains” versus “PR built-in gains,” the best practice is to take a snapshot of the asset price on the day you moved. You cannot import non-PR built-in gains to Puerto Rico and treat those gains as Puerto Rican-sourced income. You can only treat appreciation on publicly traded securities in excess of the amount in non-PR built-in gains as Puerto Rican-sourced income.

- Privately held business interest (non-marketable) – to determine the amount of “non-PR built-in gains” versus “PR built-in gains,” the investor is responsible for setting the valuation. The investor would apportion the gain as either non-PR or PR based on the numbers of days the asset has been held in each location. In other word, this calculation is the percentage of all days the individual has held the asset as Puerto Rican–sourced income while living in Puerto Rico.

How do you get the tax exemption decree?

The individual needs to submit an application to the Office of Industrial Tax Exemption (OITE) of Puerto Rico to obtain a tax exemption decree, which provides the full details of the tax rates and conditions mandated by the Act. This decree is considered a contract between the government of Puerto Rico and the individual investor. Once the individual investor obtains the tax exemption decree, the benefits granted are secured during the term of the decree, irrespective of any changes in the applicable Puerto Rico tax laws. The decree is initially valid for 15 years and can be extended for an additional 15 years.

How much does Act 60 cost?

- Application fee: $5,005

- Acceptance fee: $105 (one-time)

- Annual donation: $10,000 donation to “nonprofit entities operating in Puerto Rico and are certified under Section 1101.01 of the Internal Revenue Code of Puerto Rico, which is not controlled by the same person who owns the decree nor by their descendants or ascendants”

- Annual compliance filing: $5005

Where is your income sourced from?

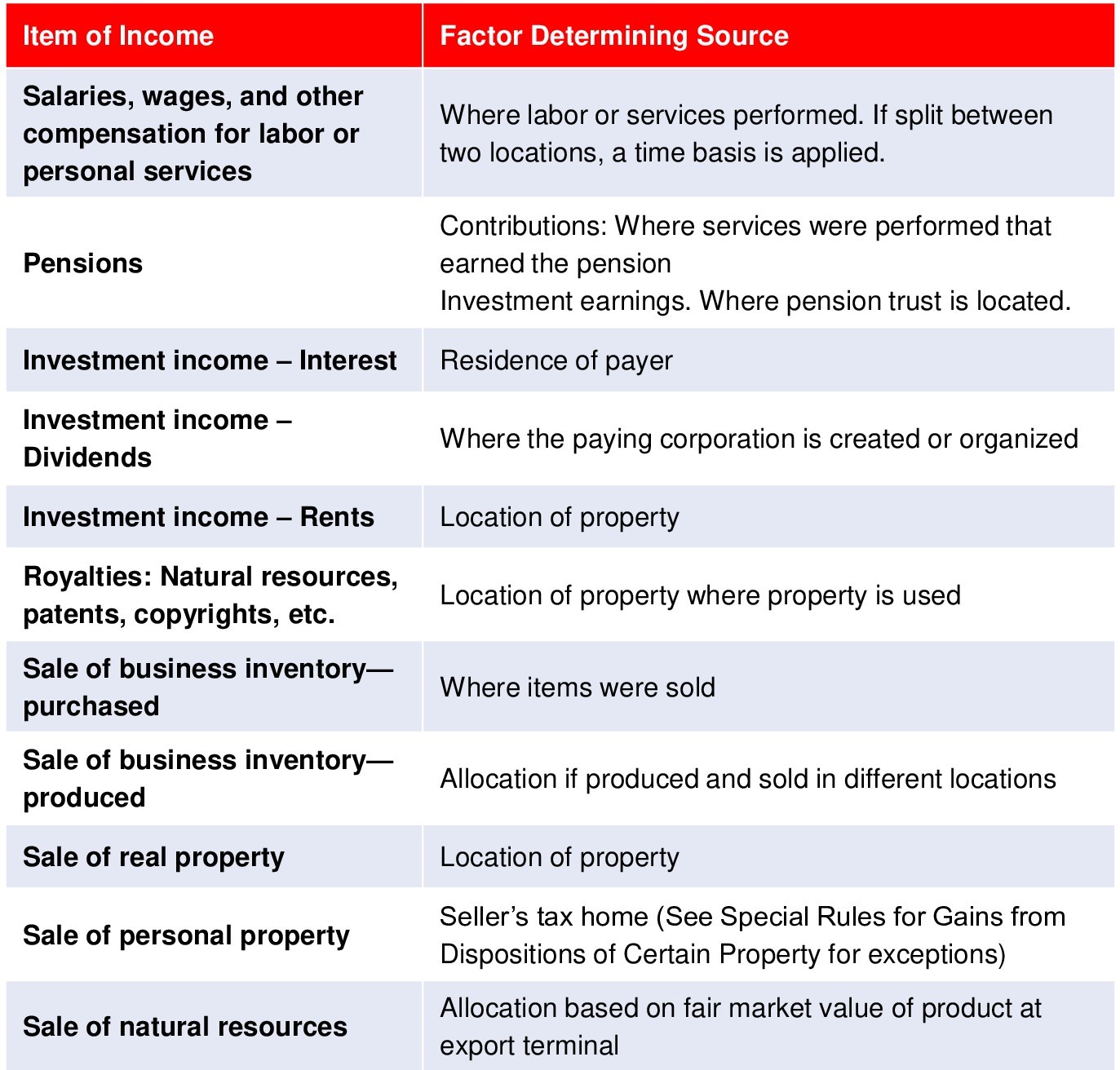

Determining where your income is sourced will dictate where you file a tax return. In determining whether Puerto Rico is right for you, and because tax rates vary, it is critical to know whether the United States or Puerto Rico has authority. In general, the rules in the United States apply to all U.S. possessions, such as Puerto Rico.

General Rules for Determining U.S. Source of Income (Resource: IRS Table 2-1)

###

Contact us to save time, money, and headaches related to your Act 60 application – you’ll thank us later.

Resource: Guide: Puerto Rico Tax Incentives Act 60

Resource: Incentives Code – Changes to Act 20 & Act 22

Disclaimer: Neither PRelocate, LLC, nor any of its affiliates (together “PRelocate”) are law firms, and this is not legal advice. You should use common sense and rely on your own legal counsel for a formal legal opinion on Puerto Rico’s tax incentives, maintaining bona fide residence in Puerto Rico, and any other issues related to taxes or residency in Puerto Rico. PRelocate does not assume any responsibility for the contents of, or the consequences of using, any version of any real estate or other document templates or any spreadsheets found on our website (together, the “Materials”). Before using any Materials, you should consult with legal counsel licensed to practice in the relevant jurisdiction.